I basically pay regarding 2% average tax price on my earnings-- and also we have almost 40K of yearly income. With little to no housing cost as well as a spent for vehicle-- that 40K goes a long means. That 2% tax does nonetheless arise from a 22% marginal tax obligation price-- 15% brace with 50 cents of SS advantage becoming taxed on the next dollar of gross income. If at the time of death, the line of credit report has actually expanded to $1.184 M as well as the residence is only worth $1M, they can create a check out of the line and also make use of the total of the line during that time. The opposite is a non-recourse car loan, suggesting there is no deficiency asserts versus the estate, the home is the only collateral for the finance.

You might also decide to rent a location so you can avoid the headaches of homeownership. Then as lengthy as you stay with your plan, you will constantly understand what you owe and also what property is offered to pass to your beneficiaries. When economic products require the Fonz or the daddy from Growing Discomforts to encourage you it's an excellent suggestion-- it possibly isn't. I'm usually not a follower of financial products pitched by former TV stars like Henry Winkler and also Alan Thicke-- as well as it's not because I as soon as had a screaming argument with Thicke. Do decline payment from individuals for a home you did not purchase. Be dubious of any individual declaring that you can have a residence without any deposit.

- If you have an existing home mortgage or HELOC, the funds you receive from a reverse home loan needs to first be made use of to pay off existing car loans secured by your home.

- The evil one is constantly in the information as well as it might not truly suffice money to move the needle for you or I, yet it's not a crazy point to do.

- So, if you're 62, have a history of long life as well as think your present place is your for life home, a reverse home loan can make good sense.

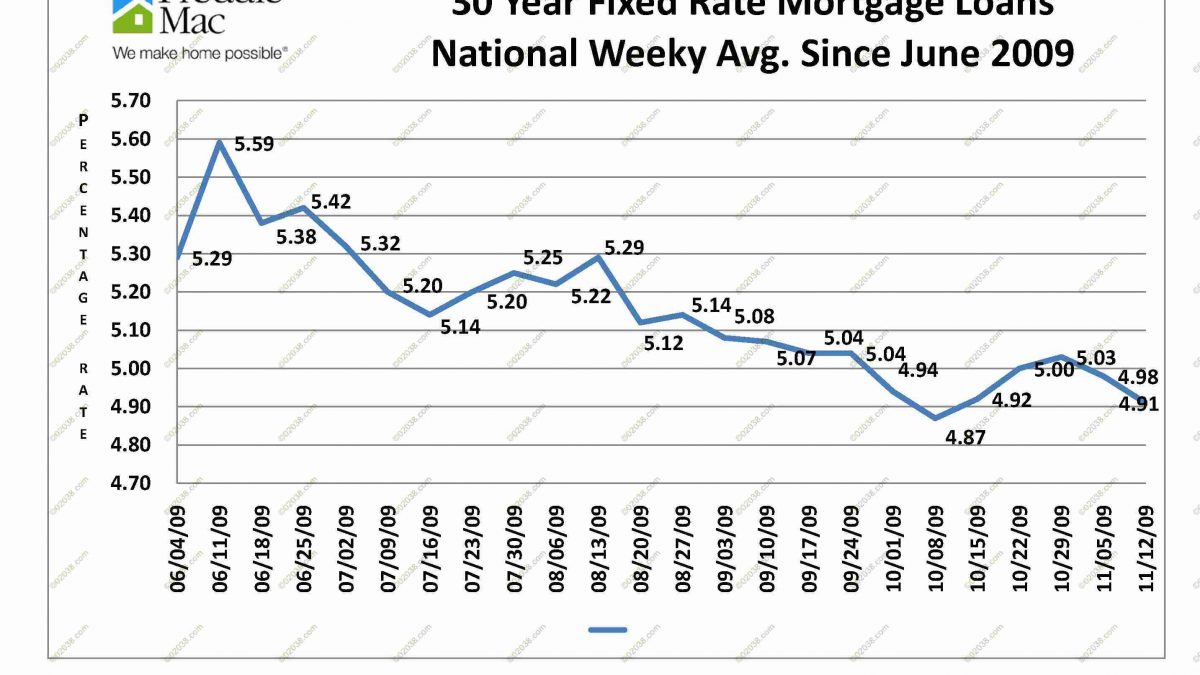

- In effect, the rate of interest charged on reverse home loans often tend to be materially greater than the rates billed on comparable kinds of loaning products such as a typical home loan or a HELOC.

- As successors, you as well as your vic donna group bro need to currently choose what is to end up being of the residential or commercial property, yet the funding must be repaid currently.

- That's due to the fact that your lending institution charges you rate of interest on your car loan balance that you remain to continue time after time.

The finance does not have to be repaid as lengthy as you live in the house. Nevertheless, the finance will end up being due when you die, stop working to pay taxes or insurance for the home, let the house fall into disrepair, or offer the wesley financial group glassdoor residence or no more use the house as your main home. The lender can not sue you or your estate for the financing balance, however it can offer the home. Never let a lender stress or rush you via the procedure. Be sure you comprehend the features as well as complete expense of a reverse home mortgage before signing anything. That changes, though, if you offer or move out of the residence, or if you pass away.

A Reverse Home Loan Is An Annuity

If you want fixed-rate funding, though, the amount of equity you can access is smaller than what you might touch with an adjustable-rate reverse Home page home mortgage. Proprietary reverse mortgages-- These are offered via personal lenders, as well as they are not subject to FHA loan restrictions. You can access your house equity without the month-to-month settlements you would find on a typical lending, like a Home Equity Line of Credit or a refinance. In fact, no settlements are called for in any way, a minimum of not till you relocate or sell your home, which is completely your choice.

Share This Tale: Is A Reverse Mortgage Worth Real Expense?

This is particularly true if he or she acts like a reverse home mortgage is a solution for all your problems, pushes you to secure a funding, or has suggestions on how you can spend the cash from a reverse home mortgage. As each month passes, the homeowner with a reverse home loan sees debt increase and equity residence equity reduction. You can never ever owe more than what your residence is worth. If your home falls in value, the reverse mortgage lender takes the loss. Utilizing home equity as retired life revenue can be a fascinating option for retiring Canadian baby boomers who have gained from solid realty markets over the past 20 years. And there's another potential reason we'll see even more passion backwards home loans.

The Bottom Line On Reverse Mortgages

Remaining in your residence might end up being unfeasible eventually in retired life if points like climbing the stairways, residence upkeep, snow elimination and also yard care end up being way too much of a burden. In this situation, you might make a decision to relocate and offer your home. The issue here is that when you do so, you should pay back the reverse home mortgage in full. Nevertheless, you might not have adequate funds to do so.